by

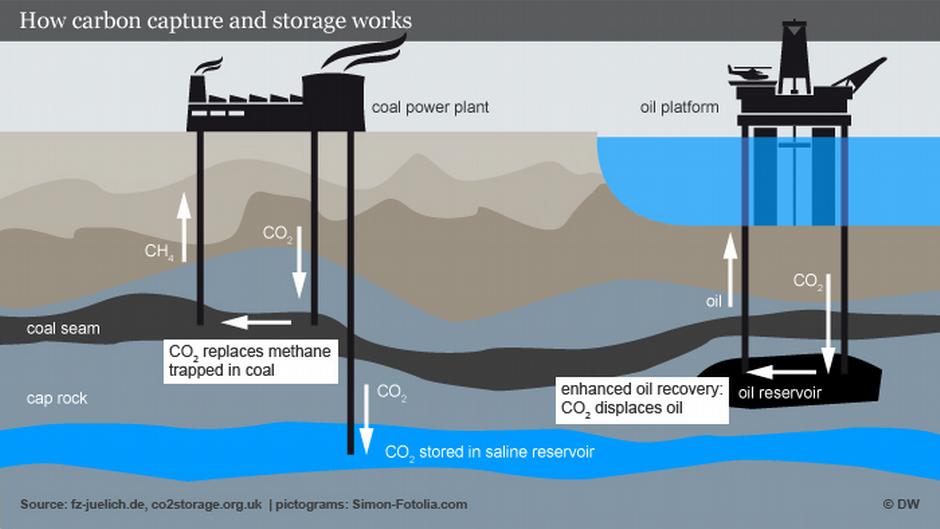

by Carbon capture and storage (CCS) is a set of technologies that can greatly reduce carbon dioxide (CO2) emissions from industrial processes and power generation. CCS involves the separation of CO2 from industrial and power plant flue gases, transporting it to a storage location and long-term isolation from the atmosphere. The captured CO2 is often stored deep underground in geological formations such as depleted oil and gas fields or deep saline aquifers. CCS is one of the few options available that can significantly reduce CO2 emissions from industrial facilities powered by fossil fuels, setting up a pathway to achieving climate neutrality goals. The global carbon capture and storage market is estimated to be valued at US$6.5 billion in 2023 and is expected to exhibit a CAGR of 4.6% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights.

Market key trends:

One of the key trends driving growth in the CCS market is the growing demand for carbon neutrality across industries. Stringent emission norms along with strong climate change policies by governments worldwide have increased investments in CCS technologies by oil & gas, cement, steel and power generation industries. For instance, the European Union’s policy framework includes targets and incentives to scale up CCS solutions across member nations. Countries like Canada, Norway and UK have implemented carbon pricing mechanisms that make CCS projects economically viable. Furthermore, initiatives like UNFCCC Paris Agreement are catalysing collaborations among nations and industries to establish regional CCS networks and storage hubs, which will help accelerate commercial deployment of carbon capture technologies on a global scale.

Porter’s Analysis

Threat of new entrants: The carbon capture and storage market has high capital requirements to enter the business and build specialized infrastructure, which deters new competition. However, supportive government policies can help lower barriers.

Bargaining power of buyers: Large corporate and industrial buyers have significant bargaining power to negotiate on project pricing and carbon credits. Their bargaining power keeps costs competitive for providers.

Bargaining power of suppliers: A few large technology providers and engineering companies dominate the supply chain. This enables them to influence pricing and contract terms.

Threat of new substitutes: No close substitutes exist currently for capturing carbon at large stationary sources. Ongoing R&D could discover alternate abatement methods.

Competitive rivalry: Major players compete intensely on technology advantages, integration expertise, project executions and value additions like monitoring services. This drives continued innovation.

Key Takeaways

The Global Carbon Capture And Storage Market Demand is expected to witness high growth over the forecast period.

Regional analysis- North America leads with many large-scale projects under operation and development. The US 45Q tax credit boosts investment. Europe follows with the European Union Emissions Trading System (EU ETS) incentivizing reductions. Developing Asia is a key growth market, especially China and India, as they seek to balance economic development and carbon goals. Supportive initiatives and carbon offset programs can accelerate regional adoption.

Key players- Leading companies in the carbon capture and storage market include Shell, Chevron, Mitsubishi Heavy Industries, Fluor, Hitachi, Aker Solutions, Honeywell, Exxonmobil and Linde. They provide integrated solutions and technologies for capture, transportation and long-term geological storage of carbon emissions. Partnerships and strategic collaborations are stepping up to address project needs across different regions.

*Note:

1. Source: Coherent Market Insights, Public sources, Desk research

2. We have leveraged AI tools to mine information and compile it